Contact Us

Contact Us Find a Broker

Find a BrokerIn this article:

")

Saving a deposit is often the biggest hurdle to buying your first home. It’s a common trope that you need a 20% deposit, but rising property prices has created a reality where the average household, earning an average income in Australia, would need to save for 5.9 years to save for a deposit for the average sized home loan. [1]

The good news is that you don’t always need a 20% deposit. Many first home buyers get into the market sooner with a 5% to 10% deposit by using government schemes or paying Lenders Mortgage Insurance (LMI).

While a typical deposit is between 5% and 20%, the right amount for you depends on your personal circumstances, eligibility for support, and overall financial strategy.

2026 Snapshot: The First Home Buyer Deposit

Recent industry data shows how first home buyers are navigating the market today.

- Typical Deposit Range: Most first home buyers aim for a deposit between 5% and 20% of the property’s purchase price. [2]

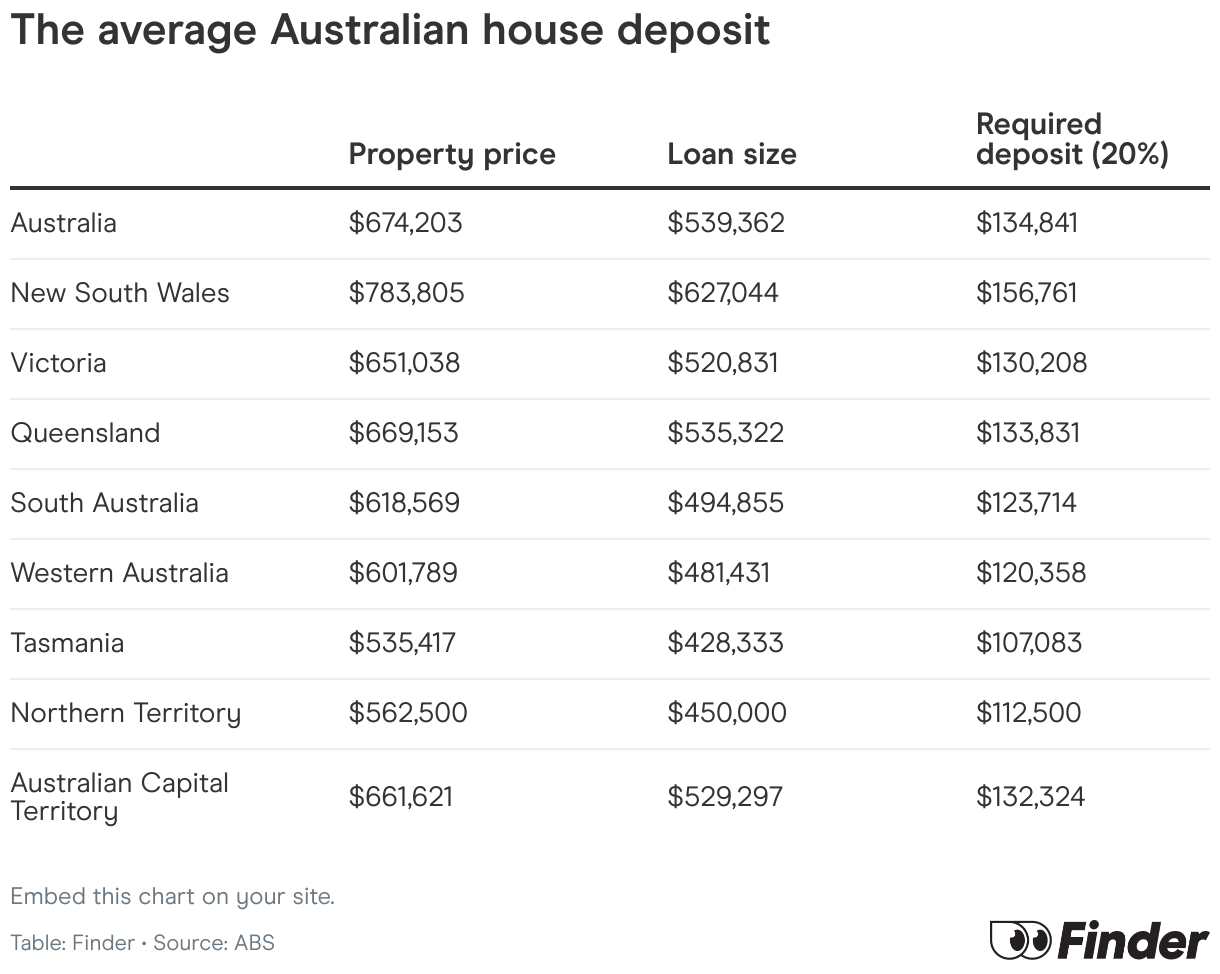

- Average Deposit Amount: The average first home buyer deposit was around $135,000 in 2025,[3] but this figure includes a wide range of circumstances across Australia.

- The “Buy Sooner” Trend: Demonstrating a shift in mindset, 70% of first home buyers in 2025 are choosing not to wait until they have saved a full 20% deposit before purchasing their home.[4]

What a 20% Deposit Really Does

Saving a 20% deposit is the traditional gold standard for a reason. It offers significant financial benefits and can make your home loan journey smoother.

The Benefits:

- Generally Avoids Lenders Mortgage Insurance (LMI): This is the biggest advantage. By having a 20% deposit from day one, you avoid paying this insurance premium, which can save significant amounts of up front costs to purchasing your first home.

- Improves Your Loan Application: A larger deposit reduces the lender’s risk, which can lead to more competitive interest rates and a wider choice of loan products.

- Provides an Immediate Equity Buffer: You start with a solid stake in your property, offering a financial cushion against potential market downturns.

The Trade-Offs:

- Time Delay: It can take years to save a 20% deposit. During this time, property prices may continue to rise, potentially costing you more in the long run.

- Opportunity Cost: While you are saving, you might also be paying rent. The money spent on rent could have gone towards building equity in your own home.

- Market Risk: If property prices increase faster than you can save, you might find yourself “chasing the market,” where your deposit goal keeps moving further away.

The Average First Home Buyer Loan Commitment

Buying with Less Than 20%

With 70% of first home buyers choosing to purchase with a smaller deposit, it’s clear that the 20% rule is no longer the only way forward. (Source: https://www.finder.com.au/insights/first-home-buyer-report-2025)

Here are some pathways to buying with a 5% to 10% deposit.

1. The 5% Deposit Scheme

This federal government initiative [insert link to previous blog] allows eligible first home buyers to purchase a property with as little as a 5% deposit without paying LMI. The government essentially guarantees up to 15% of the loan, removing the need for LMI.

- Pros: Saves you thousands on LMI and gets you into the market sooner.

- Cons: Strict eligibility criteria, including income caps and property price thresholds, and limited places are available each financial year.

- Who it suits: Eligible single or couple first home buyers who have a 5% deposit saved but want to avoid the cost of LMI.

2. A Guarantor Loan (Family Guarantee)

The Bank of Mum and Dad is a term often used to refer to a situation where a family member (usually a parent) uses the equity in their own home as additional security for your loan. This allows you to borrow up to 100% of the property value in some cases, covering both the deposit and upfront costs.

- Pros: Lets you buy with little to no cash deposit and avoid LMI entirely.

- Cons: Puts your guarantor’s property at risk. It requires careful legal and financial advice for all parties.

- Who it suits: Buyers with strong family support and a guarantor who understands and accepts the risks involved.

3. A Standard Loan with LMI

This is the most common route for those with less than 20%. You take out a standard home loan and pay for Lenders Mortgage Insurance.

- Pros: Allows you to buy a home much sooner than if you waited to save 20%.

- Cons: LMI can be a significant upfront cost, often added to your total loan amount.

- Who it suits: Buyers who don’t qualify for government schemes or have a guarantor, but have a secure income and want to enter the property market now.

How Much Cash Do You Actually Need?

Your deposit is just one piece of the puzzle. You also need to budget for several other upfront costs to complete the purchase:

- The Deposit: The percentage of the purchase price you are contributing (e.g., 5%, 10%, or 20%).

- Stamp Duty: A state government tax on the property purchase. First home buyers may be eligible for concessions or exemptions.

- Upfront Costs: These include legal and conveyancing fees, building and pest inspection reports, loan application fees, and moving costs. A good rule of thumb is to budget around 3-5% of the purchase price for these expenses.

- Buffer: It’s wise to have an extra buffer of savings for unexpected expenses after you move in.

For example, on a $700,000 property, a 20% deposit is $140,000. With a 10% deposit ($70,000) or a 5% deposit ($35,000), you would also need to account for stamp duty (if applicable), solicitor or conveyancer fees and other costs, plus the LMI premium if you’re not using a government scheme. The total cash needed will vary greatly, which is why speaking to a mortgage broker is so important.

Saving Faster (and Smarter)

Boosting your savings rate can significantly shorten your timeline to home ownership.

- First Home Super Saver Scheme: Make voluntary contributions to your superannuation to save for a deposit, benefiting from a lower tax rate.

- Automate Your Savings: Set up an automatic transfer to a high-interest savings account on payday.

- Audit Your Expenses: Review your bank statements to identify where you can cut back on non-essential spending.

- Increase Your Income: Consider a side hustle or taking on extra work to accelerate your savings.

- Use Windfalls Wisely: If you receive a bonus, tax refund, or cash gift, put it directly towards your deposit.

The LMI Basics

Lenders Mortgage Insurance (LMI) often sounds complicated, but the concept is simple. It’s an insurance policy that protects the lender (not you) if you are unable to repay your loan.

You are typically required to pay LMI if your deposit is less than 20% of the property’s value. While it is an extra cost, it can be a valuable trade-off to enter into the property market sooner.

It allows you to secure a property years earlier than you otherwise could, giving you a foothold in the market.

The cost of LMI can often be added to your total loan amount, so you don’t always need to pay it as an upfront lump sum.

Your Next Step

Navigating deposit requirements, government schemes, and loan products can be overwhelming. Each lender has different policies, and the best path for you is unique.

A Yellow Brick Road mortgage broker can help you create a clear plan. We will review your financial situation, explain your options, and help you get pre-approved so you can start searching for your home with confidence.

We’ll get you sorted. Contact a local Yellow Brick Road mortgage broker today for a no-obligation chat.

[2] https://www.finder.com.au/insights/first-home-buyer-report-2025

[4]https://www.finder.com.au/insights/first-home-buyer-report-2025