Contact Us

Contact Us Find a Broker

Find a BrokerIn this article:

")

Key Takeaways:

- Market Shift: Properties priced under the Home Guarantee Scheme caps are growing in value significantly faster than higher-priced homes.

- The Numbers: In the December quarter alone, homes under the price cap grew by 3.6%, compared to just 2.4% for those above it.

- Driving Forces: High interest rates are pushing more buyers, including investors, towards affordable properties, increasing competition.

For many Australians, the dream of owning a home is tied to affordability. We all know that getting a foot on the property ladder is challenging, especially with the cost of living pressures we face today. But a new trend has emerged that is reshaping the market, particularly for those looking at entry-level properties.

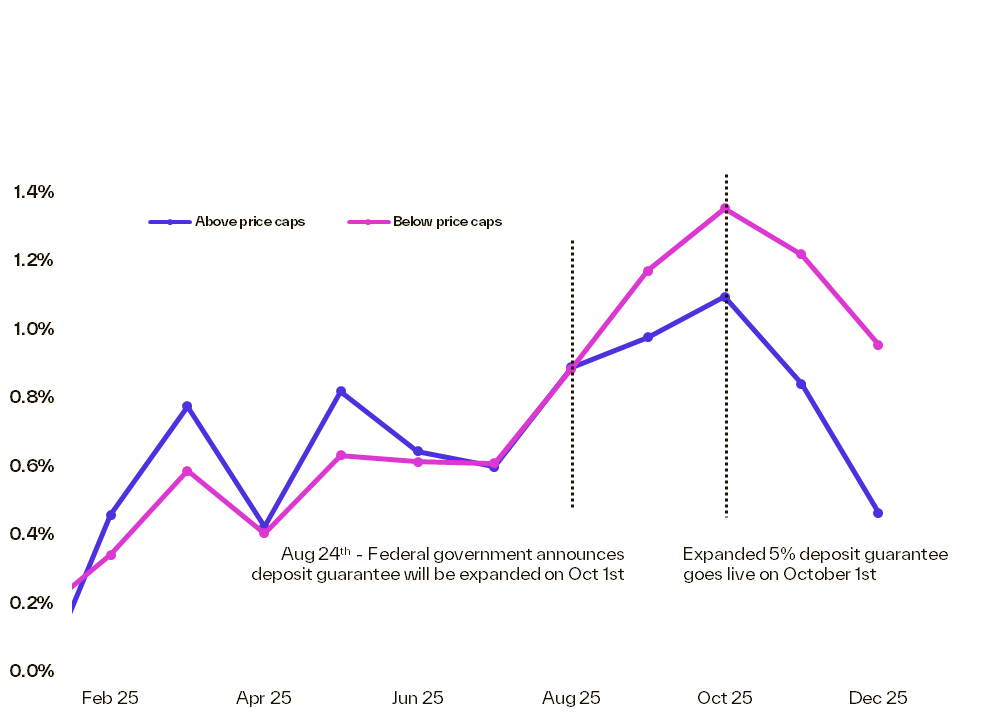

Recent data reveals that the very scheme designed to help first home buyers, the 5% Deposit Scheme, is influencing property values in perhaps unexpected ways. Lower-priced homes, specifically those falling under the scheme’s price caps, are now recording stronger growth than their more expensive counterparts.

The Rise of the ‘Affordable Home’

Since late last year, a distinct gap has opened up in the Australian property market. New research by Cotality indicates that homes valued below the Home Guarantee Scheme price caps are outperforming the broader market.

In the December quarter of 2025, dwelling values for properties under the cap rose by 3.6%. In contrast, properties priced above the cap grew at a more modest 2.4%.

This suggests that demand is concentrating heavily at the affordable end of the spectrum. While the top end of the market cools, the entry-level segment is heating up. For first home buyers, this is a double-edged sword: the government support is there to help, but the competition for eligible properties is intensifying.

“The expanded 5% deposit guarantee has sharpened demand at lower price points, with under‑cap markets outperforming across almost nine‑in‑ten regions,” said Tim Lawless, Cotality’s research director.

“We’re seeing a clear shift in momentum, with buyers increasingly targeting homes that fall under the new price caps.”

“This trend was already visible before the scheme’s official start on October 1, suggesting some buyers acted early to secure properties before competition increased.”

Competition Increasing

It may not be just the Home Guarantee Scheme driving this demand. It’s a combination of factors creating a perfect storm for lower-priced properties.

1. Serviceability Constraints

Borrowing capacity has been squeezed for a number of years since the post-Covid era rate hike environment took off.

Many buyers who might have previously looked at purchasing properties at prices under the previous Government Schemes, which had low property price caps, may now be adjusting their expectations and targeting homes with increased purchase prices. This is in an elevated rate environment, making serviceability a trickier task for first home buyers.

2. Investors Are Back

It’s not just first home buyers competing for these properties. Investors are currently very active, comprising roughly 41% of mortgage demand in the third quarter. Investors, chasing better rental yields and lower entry costs, are targeting the same stock as first home buyers, adding another layer of competition.

3. Fear of Missing Out

The expansion of the Government’s 5% scheme and the anticipation of rising prices have encouraged many buyers to act early. Previously, the government’s scheme was limited to 10,000 places per year for eligible applicants, with income caps in place. Under the new scheme, places are unlimited and income caps have been removed. People who might have waited are jumping in now to secure a property before values climb further out of reach.

A Tale of Two Markets

This trend isn’t isolated to one pocket of the country; it is consistent across almost every capital city and regional market (with the exception of the ACT). However, the divide is most stark in our biggest city.

Sydney is currently the clearest example of this two-speed market. Cotality identified that in the December quarter:

- Homes valued under the cap rose by 2.3%.

- Homes valued above the cap actually fell by 0.1%.

This data highlights that while the premium end of town might be softening, the battle for affordability is keeping prices robust in the entry-level market.

What Does This Mean for You?

If you are a first home buyer, this data underlines the importance of being prepared. The properties you are likely targeting (those under the price caps) are currently some of the most sought-after assets in the country.

Waiting on the sidelines in a market like this can be risky. If prices in the lower bracket continue to grow at 3.6% per quarter, a property that is affordable today might exceed the price cap (or your borrowing capacity) in time.

However, you don’t have to navigate this competitive landscape alone.

We’re Here to Help

In a market where affordable properties are moving fast, having a trusted expert in your corner can make all the difference.

At Yellow Brick Road, our mortgage brokers understand the local dynamics of your community. We can help you:

- Assess your eligibility for the 5% Deposit Scheme.

- Determine your true borrowing power so you can act quickly when you find the right home.

- Compare loans from a wide panel of lenders to ensure you’re getting a competitive rate.

We know that every Australian’s financial situation is unique. Don’t let market competition push your dreams out of reach. Reach out to us today to get started.

Disclaimer: The information provided in this article is general in nature and does not constitute financial advice. It has been prepared without taking into account your objectives, financial situation, or needs. Before acting on this information, you should consider its appropriateness having regard to your own circumstances. Eligibility for government schemes is subject to criteria and lender approval.